World indices overview: news from US 30, US 500, US Tech, JP 225, and DE 40 for 15 May 2025

US inflation data and tariff agreement with China gave investors hope; now it is up to the Federal Reserve to make the next move. Find out more in our analysis and forecast for global indices for 15 May 2025.

US indices forecast: US 30, US 500, US Tech

- Recent data: the US CPI was 2.3% in April

- Market impact: hopes for a soft landing in the economy are growing, which is generally positive for the broad market, especially for cyclical and consumer companies

Fundamental analysis

US annual inflation eased to 2.3% in April, below forecasts of 2.4%, marking the lowest level since the beginning of 2021, while the core CPI remained at 2.8%, with both indices up 0.2% month-on-month. The softer-than-expected data reduces pressure on the Federal Reserve to tighten monetary policy further – the US dollar has weakened – and boosts hopes for an earlier rate cut if tariffs do not derail the disinflation process.

Investors will now focus on Friday’s PPI data and the Federal Reserve’s comments for clues on the future policy direction. Technology and growth stocks, alongside real estate, may get a boost from lower financial costs.

US 30 technical analysis

The US 30 approached the 42,535.0 resistance level. As long as the 37,060.0 support level remains intact, the price may get stuck in a sideways range. However, it should be noted that the index recouped losses since early April 2025 during a local correction.

The following scenarios are considered for the US 30 price forecast:

- Pessimistic US 30 forecast: a breakout below the 37,060.0 support level could push the index down to 35,060.0

- Optimistic US 30 forecast: a breakout above the 42,535.0 resistance level could drive the index to 43,890.0

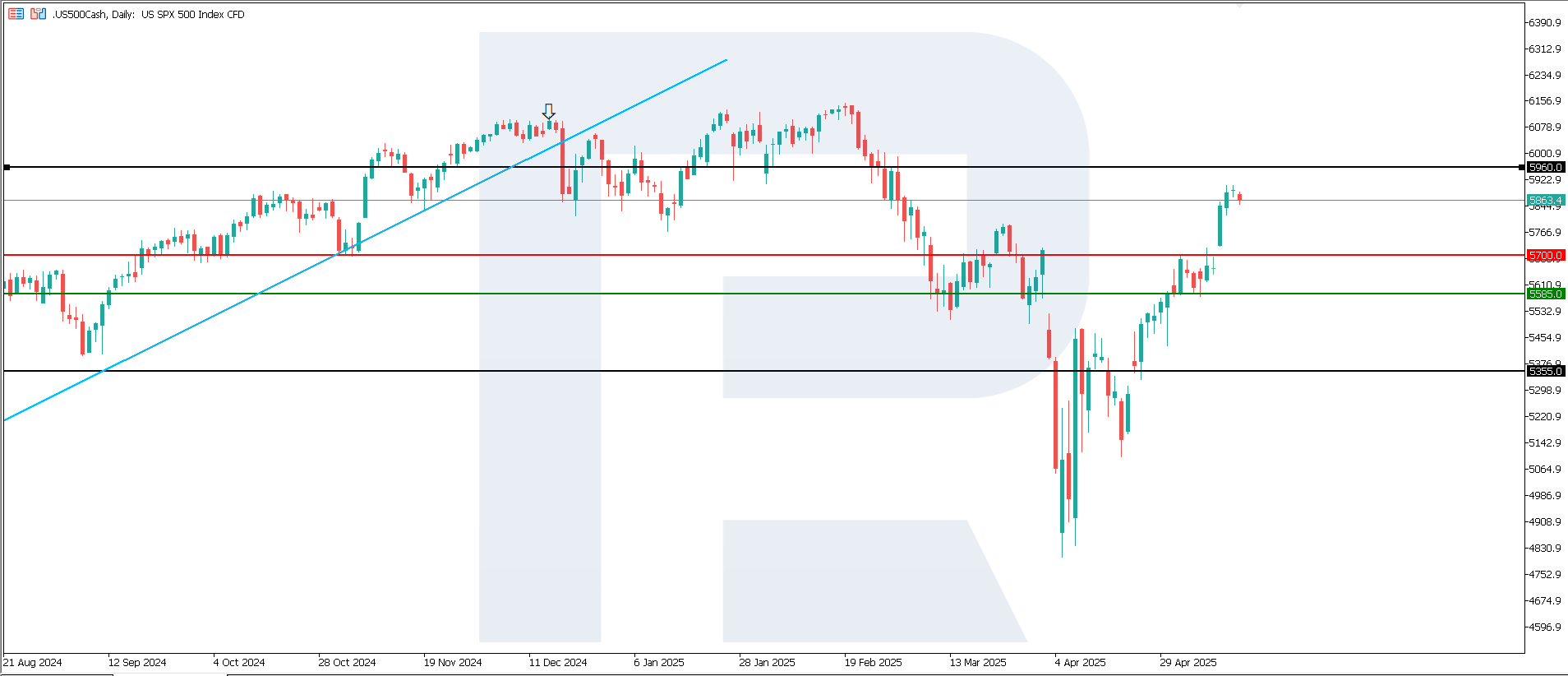

US 500 technical analysis

The US 500 index rose for the first time this year. After the longest winning streak, prices are correcting while remaining within an uptrend. The support area has shifted to the 5,585.0 mark, with the resistance level yet to form after a breakout above resistance at 5,700.

The following scenarios are considered for the US 500 price forecast:

- Pessimistic US 500 forecast: a breakout below the 5,585.0 support level could send the index down to 5,355.0

- Optimistic US 500 forecast: if the price consolidates above the previously breached resistance level at 5,700.0, the index could climb to 5,960.0

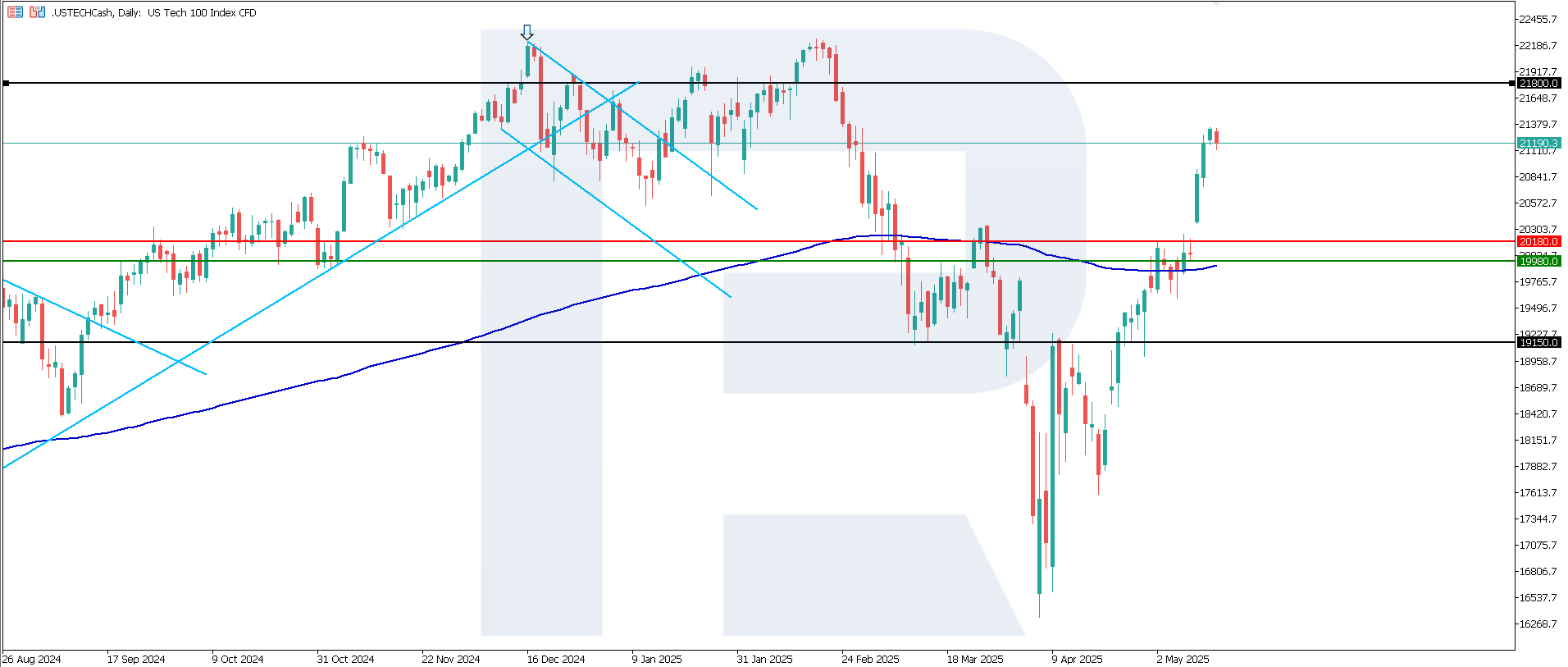

US Tech technical analysis

The US Tech index broke above the 20,180.0 resistance level, while the support area shifted to 19.980,0. The price consolidated above the 200-day Moving Average, which is typically seen as a technical sign of a renewed uptrend.

Scenarios for the US Tech index price forecast:

- Pessimistic US Tech forecast: a breakout below the 19,980.0 support level could push the index down to 19,150.0

- Optimistic US Tech forecast: if the price consolidates above the previously breached resistance level at 21,180.0, the index could rise to 21,365.0

Asian index forecast: JP 225

- Recent data: Japan’s current account totalled 3.68 trillion JPY in April

- Market impact: a weaker yen traditionally supports exporters’ stock prices

Fundamental analysis

The surplus of 3.678 trillion JPY means that Japan earned nearly 3.7 trillion JPY more in net exports and investment income in April than it spent on imports and payments to non-residents. This decline from 4.061 trillion in March indicates a relatively weaker external demand or higher import costs.

Investors see the current account surplus as a margin of safety for the economy as it shows that the country earns more from the world than it spends. A narrowing surplus raises questions about the pace of global demand and may increase market volatility, especially in exporter stocks and securities.

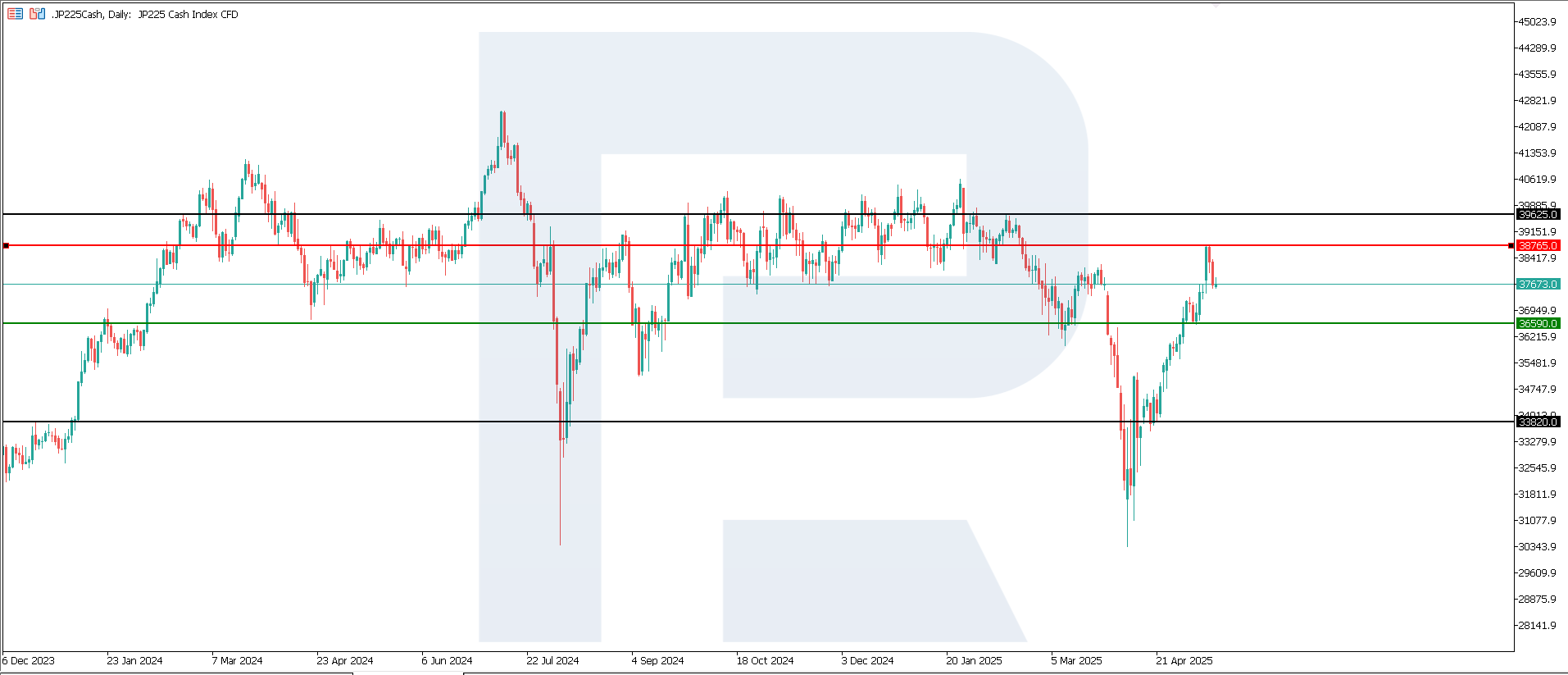

JP 225 technical analysis

The JP 225 index broke through a medium-term sideways channel. Despite a prevailing downtrend, the price breached the 38,130.0 resistance level. This breakout could be false. A new resistance level formed at 38,765.0, with the trend reversing upwards.

The following scenarios are considered for the JP 225 price forecast:

- Pessimistic JP 225 forecast: a breakout below the 36,590.0 support level could push the index down to 33,820.0

- Optimistic JP 225 forecast: a breakout above the 38,765.0 resistance level could propel the index to 39,625.0

European index forecast: DE 40

- Recent data: the German CPI came in at 2.1% in April

- Market impact: such robust data indicates a stronger economy and may boost market confidence

Fundamental analysis

The data in line with forecasts and easing annual inflation reduce the pressure on the ECB to tighten credit, creating favourable conditions for rate-sensitive stocks (technology and real estate). A moderately steady CPI allows banks to expect to maintain current margins without sharp interest rate fluctuations.

Stable inflation strengthens the euro against other currencies, potentially making exporters slightly less competitive, but with moderate CPI growth, the negative effect will be insignificant. Overall, the CPI data remains in a comfortable area for the market, as it does not require the ECB to take emergency actions and supports balanced and moderately bullish dynamics of German stocks.

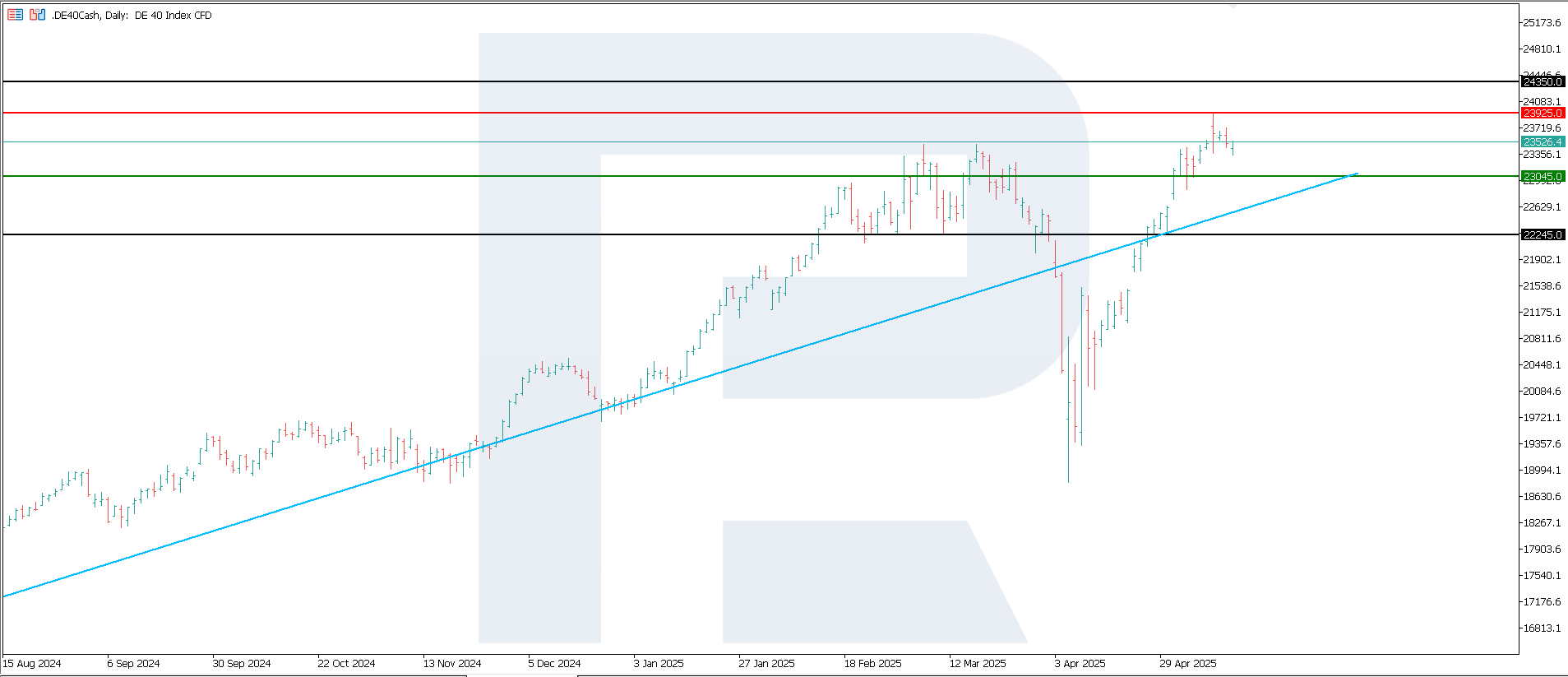

DE 40 technical analysis

The DE 40 stock index broke above the 23,435.0 resistance level, with the support line shifting to 23,045.0 and new resistance forming at 23,625.0. A new growth cycle could begin, with the potential to reach a new all-time high.

The following scenarios are considered for the DE 40 price forecast:

- Pessimistic DE 40 forecast: a breakout below the 23,045.0 support level could push the index down to 22,245.0

- Optimistic DE 40 forecast: a breakout above the 23,625.0 resistance level could boost the index to 24,345.0

Summary

Most global stock indices experience upward momentum, with the US 500 rising for the first time since the beginning of 2025. The US 30 failed to break above the resistance level. Amid easing inflation in the US and the EU, investors will be awaiting comments from regulators – the Fed and the ECB. In addition, all eyes will be on talks between the US and the EU on reciprocal tariffs.

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews.